Business & Tech

Sammamish Homebuyers: Interested in Learning About Credit Scores?

Sammamish Patch real estate columnist looks at the topic and how they affect homebuyers, especially with new regulations.

Consistent through all new regulations to finance a home is a requirement for a higher credit score. Although historically higher credit scores always helped lower rates and fees that the buyer had to pay, it is even more important today, where funds are limited, to find ways to improve and maintain a good score.

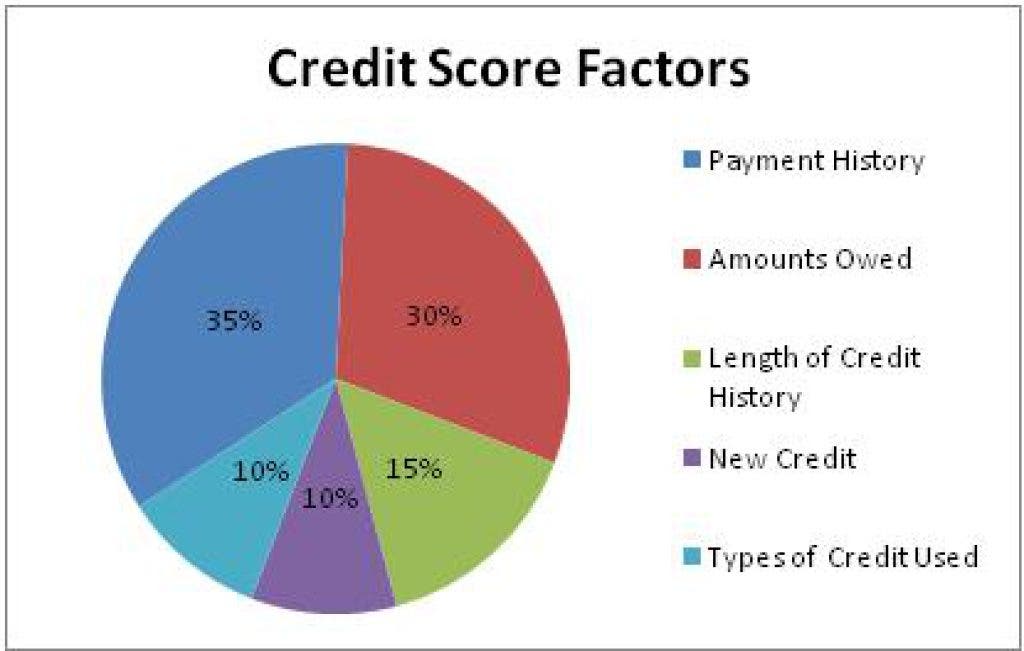

Credit bureaus evaluate five areas to determine credit worthiness. Most of us do not understand what those factors are or what value is placed on each of them.

Payment History

Interested in local real estate?Subscribe to Patch's new newsletter to be the first to know about open houses, new listings and more.

On top of this list is late payments. Consistency is crucial. Collections, repossessions, foreclosures, tax liens, bankruptcies and judgments are all considered.

Amounts Owed

Interested in local real estate?Subscribe to Patch's new newsletter to be the first to know about open houses, new listings and more.

Credit cards seem to be the most problematic. It is not necessarily how much you owe, but the amount of credit you have. If you owe $2,000 on a credit card with a limit of $2,500, your score will be lower than if you owe $8,000 on a credit card that has a limit of $30,000. It is the same scenario with HELOC (Home Equity Line of Credit) and installment loans. Having a low balance highlights the fact that you are financially responsible. Sandy Collins, a mortgage Broker with Key Bank, recommends when applying for a line of credit to request more than is needed. Of course, not using the extra balance is important.

Length of History

History starts the first day you apply for a loan. Two years of history will not get you an 800 score but being responsible overtime will make buying easier.

New Credit

Even good scores may be affected by applying for several credit cards at the same time. But, every time your credit is checked does not mean that your score will go down.

Too many inquiries may have a negative impact on your credit score. However, most recently developed credit scores recognize when a consumer is shopping for the best rates and either ignore multiple inquiries or count them as only one inquiry if they occur within a specific period of time. In such cases, shopping around will have little or no impact on a credit score.

Types of credit

Evaluators look to see where the credit is coming from. Having all debt on credit cards is generally not looked upon favorably. Installment loans, mortgage or car payments, provide an accurate history of payments.

Buying a home is not the only thing affected by a low credit report. Every major purchase could be affected. Even an employer for a job application could consider a credit report an important part of the hiring process.

How can you protect yourself? These four steps may be obvious but many of us do not take the initiative to monitor our credit scores.

Step 1 – Order credit reports and scores. The first step is for borrowers to get a complete picture of their current credit situation by ordering a copy of their credit reports from all three national credit bureaus.

Step 2 – Verify the data being reported. It is the consumer’s responsibility to verify the accuracy of all data in the report.

Step 3 – Dispute any inaccurate information. Contact creditors and send letters of dispute to the credit bureaus. These letters must be sent certified mail. Be persistent. Collins added: “The most common credit problems are sometimes the easiest to correct. Judgments for minor things such as a parking ticket that was not paid are listed on your report by the court. Removing it only takes a letter to the court, but if you don’t know it is there, your application for a home loan could be turned down or delayed.”

Step 4 – Pay your bills on time and keep the balances on credit cards low.

Don’t be surprised! A little foresight may make all the difference in the ability to move into that perfect home.

Steve Tedrow, branch manager at Windermere Mortgage Services, gave buyers with less than stellar credit some hope when he stated: “Even if you have less than perfect credit, there are still safe, secure mortgage financing options available. Reputable mortgage lenders employ knowledgeable mortgage consultants who can evaluate your financial situation and help you get the financing you need to fit your budget.”

Credit scores go a long way in determining what you will pay for a loan. These are just examples of the differences.

This is based on a $300,000 fixed rate mortgage. Source: MyFICO.com

FICO Score APR (Annual Percentage Rate) Monthly Mortgage Payment 760-850 4.645% $1,546 700-759 4.867 $1,586 680-699 5.044 $1,619 660-679 5.25 $1,658 640-659 5.688 $1,739 620-639 6.234% $1,844Joan Probala is the managing broker for Issaquah Windermere (Windermere Real Estate/East Inc.). She has 30 years of experience in real estate, construction and sales.